Circle's Acquisition of Axelar Sparks Controversy: AXL Plunges 15% as Long as People Don't Want Coin

Original Article Title: "Circle's Acquisition of Axelar Sparks Controversy: Giant Only Wants People, Not Coin"

Original Article Author: Azuma, Odaily Planet Daily

In the early morning of December 16th, stablecoin giant Circle officially announced that it has completed the signing of an agreement to acquire the core team and technology of Interop Labs, the initial development team of the cross-chain protocol Axelar Network. This move is intended to advance Circle's cross-chain infrastructure strategy and support Circle in achieving seamless and scalable interoperability on its core products such as Arc and CCTP.

This was supposed to be another typical case of an industry giant acquiring a high-quality team, seemingly a win-win situation. However, the key issue lies in the fact that Circle explicitly mentioned in the acquisition announcement that this transaction only involves the Interop Labs team and its proprietary intellectual property, while Axelar Network, the Axelar Foundation, and the AXL token will continue to operate independently under community governance. The other contributing team of the original project, Common Prefix, will take over the relevant activities of Interop Labs.

In simple terms, Circle took away Axelar Network's original development team but explicitly excluded Axelar Network itself and its token AXL.

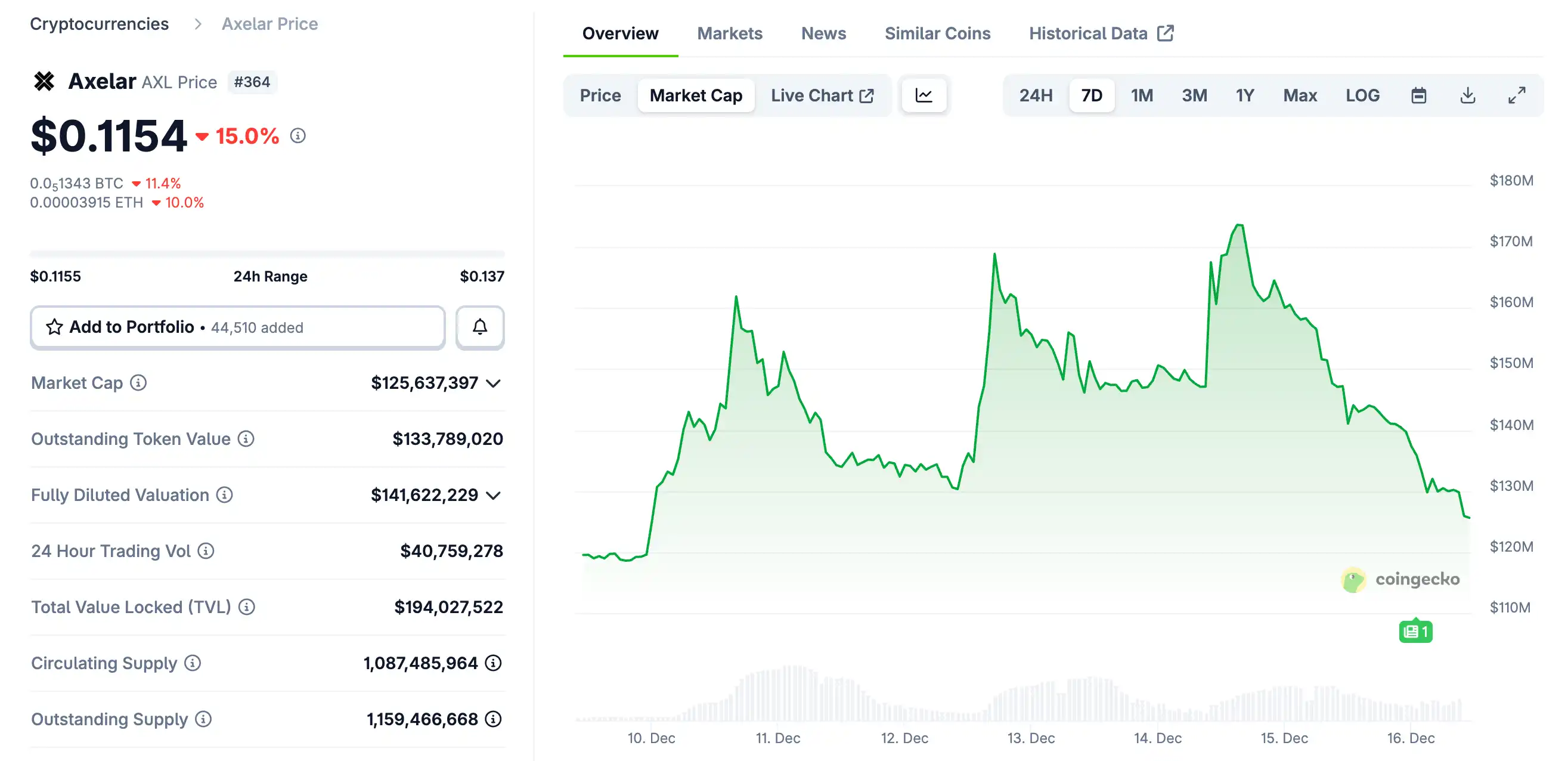

Impacted by this sudden news, AXL experienced a sharp drop, trading around $0.115 as of approximately 10:00 AM this morning with a 24-hour decline of 15%.

At the same time, the unique situation of the acquisition itself, characterized by "wanting people but not coin," and the ensuing "Equity vs. Token" issue, has sparked numerous discussions within the community, with proponents and opponents of this type of acquisition model holding differing views and engaging in heated debates.

Opposing Viewpoint: Implicit RUG, Chaos by Circle, Only Token Holders Are Hurt

A key force within the opposing camp consists of some VCs, which is not hard to understand—"I invested real money in the project's token equity, held a substantial amount of the token, and now you take away the ones doing the work - what good is this token to me?"

Simon Dedic, Founder of Moonrock Capital, commented on this: "Another acquisition, another RUG. Circle acquires Axelar but explicitly excludes the foundation and AXL token, this is simply a criminal act. Even if it does not violate the law, it goes against ethics. If you are a founder looking to issue a token: either treat it like equity or get lost."

The Block Co-founder and 6MV Founder Mike Dudas commented, "For those who think this is a token vs. equity issue, I can tell you definitively that this is all Circle's doing. There are rumors that Circle's VP of Corporate Development once told a co-founder of Axelar, 'I don't care about your investors,' and without paying any consideration to investors, 'bought' the CEO and IP out from under them, which are crucial to Arc's launch."

Lombard Finance Founder posted Axelar's trend and predicted, "Axelar's core team has been bought by Circle, and AXL may now be worthless. The token has been issued for over three years, the team's equity has already been fully cashed out. Yet, the result is very uncomfortable: the team and/or investors sold tokens for profit, while token holders can only hope for a distant dream."

ChainLink community figure Zach Rynes stated, "This once again exposes the token vs. equity conflict of interest issue plaguing the crypto industry. The development team behind the protocol has been successfully acquired, while token holders who funded that team have received nothing. The so-called continued independent operation under community governance is no different from the development team abandoning users for a better future. If we want to attract real capital, this is the industry's top issue that needs to be addressed."

SOAR Ecosystem Lead Nicholas Wenzel said, "The Axelar token is heading towards zero, thanks for participating. This is another case of token holders gaining nothing while equity holders profit handsomely from the acquisition."

Supporting Viewpoint: Normal Market Behavior, Tokens are inherently at the bottom of the capital structure

If the opposing side focuses more on the unfair treatment of token holders, the supporting side will focus more on the market rules of financing and M&A.

Arca Chief Investment Officer Jeff Dorman believes Circle's actions are fair and explains in detail the capital structure of corporate financing and the natural disadvantage tokens find themselves in.

Businesses raise funds through different levels of the capital structure, and these levels inherently have a clear priority order, with some levels naturally ahead of others — secured debt > unsecured senior debt > subordinated debt > preferred shares > common shares > tokens.

Throughout history, there have been countless cases where the interests of one type of investor have been achieved at the expense of another type of investor.

· In bankruptcy liquidation, creditors succeed at the expense of equity investors;

· In leveraged buyouts (LBOs), equity holders often profit at the expense of debt holders;

· In take-unders, creditors usually have priority over equity holders;

· In strategic acquisitions, both creditors and equity holders usually benefit (but not always);

· And tokens are often at the bottom of the capital structure…

This does not mean that tokens have no value, nor does it mean that tokens necessarily need some kind of "protective mechanism," but the market needs to recognize a reality: when a company acquires another company of already low value, and the tokens issued by that company are virtually worthless, token holders will not magically receive a "unicorn dividend." In such cases, equity returns are often achieved at the expense of token losses.

Avichal Garg, Co-Founder of Electric Capital, also commented: "This is a normal phenomenon. If all future value is created by the team, then there is no company willing to pay returns to investors."

Core Contradiction: What Exactly Are Tokens?

Amid the "talent over tokens" acquisition controversy between Axelar and Circle, both sides of the debate seem to have valid points.

The anger of the opposition is real: Token holders took on risk at the project's most challenging and critical liquidity and narrative support stage, only to be completely excluded at the key value realization point. From the outcome perspective, the core team and intellectual property have achieved value realization, while the tokens have been left in a narrative vacuum of "community governance," and the market has provided the most direct vote through price, which has indeed left all believers in token value deeply frustrated.

The judgment of the supporters also has practical rationality: From a strict capital structure standpoint, tokens are neither debt nor equity, naturally lacking priority in the context of mergers and liquidations. Circle did not violate existing business rules; it simply made a calculated decision based on the assets most valuable to itself.

The true core of the contradiction lies not in whether Circle is ethical, but in an issue that has long been deliberately avoided by the industry: What exactly is a token in the legal and economic structure?

During optimistic times, tokens were assumed to be "quasi-equity," endowed with the imagination of claiming success in the future; however, in real scenarios such as mergers and acquisitions, bankruptcy, and liquidation, they were quickly reduced to their original form of "non-equity instruments." This narrative-based equity and the underlying structure are the root causes of the repeated conflicts.

The Axelar acquisition case may not be the last of such controversies, but hopefully, it can serve as an opportunity for the industry to further contemplate the positioning and significance of tokens—Tokens do not inherently possess rights; only rights that have been institutionalized and structured will be recognized at crucial moments. The specific implementation still requires all industry participants to explore and practice together.

You may also like

Morning Report | CoinEx becomes a key hub for Iran to evade sanctions, involving over $3.8 billion in funds; Kalshi seeks a new round of financing, with a valuation potentially rising to $40 billion

From the white-haired stock god to the billionaire fund mogul, the smart people shorting Nvidia are all getting rich using the same framework

Why do cryptocurrency projects always like to change their names?

Global Launch: As predictions become the most scarce asset in the AI era, Manadia is defining the next generation of the value internet

Who is footing the bill for the $64 billion accounting frenzy?

I never expected that the first application of AI x Crypto would be in security auditing

What is your view on Binance's competitive advantages?

ETH has entered a non-consensus phase, and the turning point is approaching!

The shift in the cloud of the air: from despising stablecoins a year ago to the high-profile entry of capital today

The survival dilemma of small and medium exchanges behind the withdrawal anomalies exposed by AscendEX

Why Is Bitcoin Falling Below $60K? 5 Key Market Drivers Explained

Bitcoin has dropped sharply amid ETF outflows, Strategy stock weakness, AI stock rallies, and changing Fed expectations. Explore the key forces driving BTC’s latest correction and what traders should watch next.

Bitcoin vs. Gold in 2026: Which Asset Performs Better in Different Markets?

Morning News | The draft amendment to the People's Bank of China Law aims to clarify the legal status of digital renminbi; South Korea will transfer about 40 unregistered virtual asset service providers to law enforcement agencies

The cryptocurrency industry has entered the "Show Me" era: merely relying on vision is no longer enough

Interpreting the Ethereum Foundation's new structure: Reaffirming self-sovereignty amid institutional trends

Former SpaceX engineer reconstructs the financial execution system using first principles

Standard Chartered Bank sings a 50x rhapsody again, aiming for AAVE to reach 3500 USD